What Lenders Really Look at When Approving a Mortgage

Buyer's Guide The Mark & Al Team February 18, 2026

Buyer's Guide The Mark & Al Team February 18, 2026

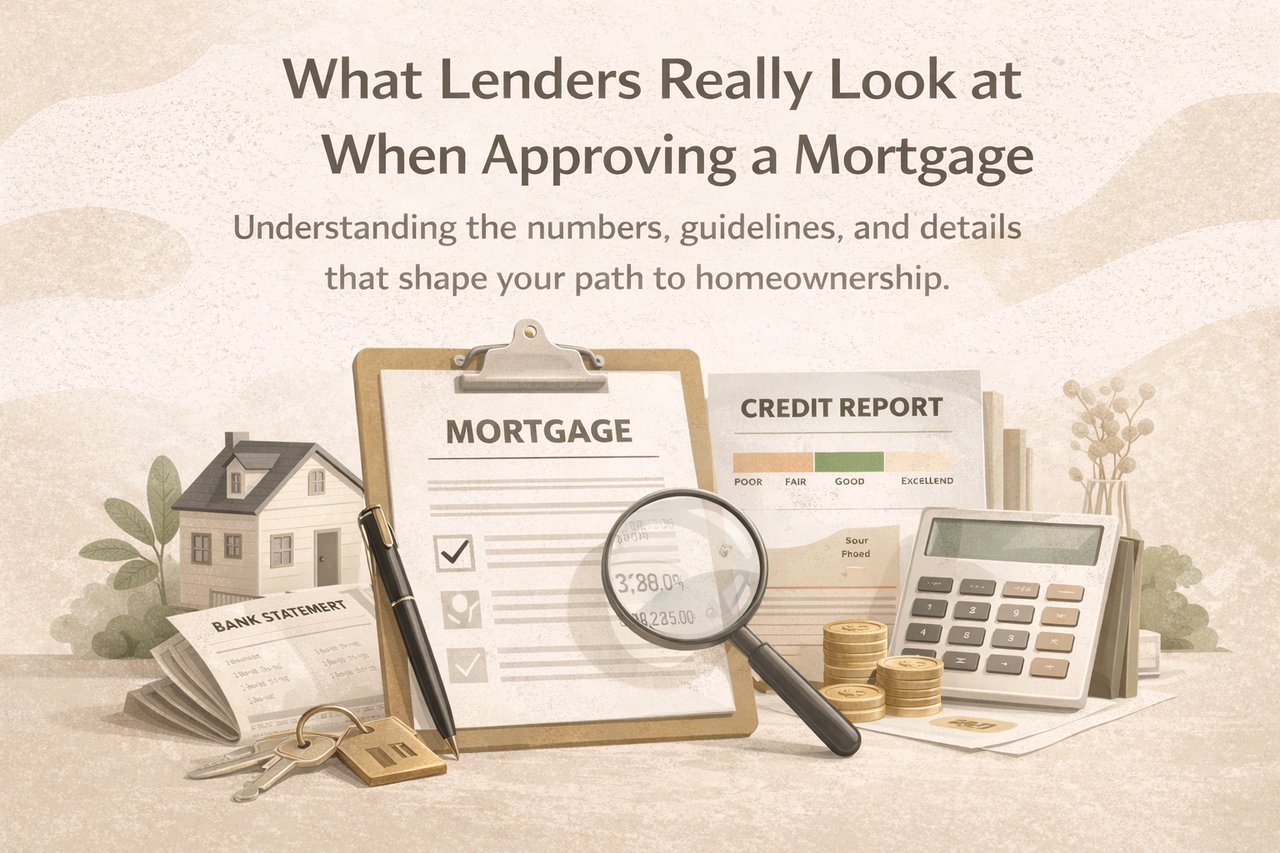

Buying a home starts long before you tour properties — it starts with financing. One of the most common questions buyers ask is: What do lenders actually look at when approving a mortgage?

Understanding the approval process can help you prepare strategically, avoid surprises, and move forward with confidence.

Here’s what really matters.

Your credit score is one of the first things a lender reviews. It gives them insight into how you’ve managed debt in the past.

In general:

Higher scores qualify for better interest rates

Lower scores may still qualify, but at higher rates

Major red flags include recent late payments, collections, or high credit utilization

Improving your score even slightly before applying can significantly impact your monthly payment.

DTI compares your monthly debt obligations to your gross monthly income.

Lenders want to see that you can comfortably handle a mortgage payment in addition to existing debts like:

Car loans

Student loans

Credit cards

Personal loans

Lower DTI = lower perceived risk.

Lenders look for consistent, reliable income. They typically review:

Two years of employment history

Recent pay stubs

W-2s or tax returns

Bonus or commission income (if applicable)

Job changes aren’t automatically a problem, but stability matters.

Beyond your down payment, lenders want to see that you have reserves — funds left over after closing.

This reassures them that you can handle:

Unexpected expenses

Temporary income changes

Emergency situations

While many buyers believe 20% is required, that’s not always the case.

Loan programs vary, and down payment requirements depend on:

Loan type

Credit profile

Occupancy type

The key is understanding which option fits your financial goals.

Yes — lenders also evaluate the home.

They will consider:

Appraised value

Property condition

Loan-to-value ratio

The property must meet lending guidelines in order for the loan to move forward.

Getting pre-approved before home shopping gives you:

Clear budget expectations

Stronger negotiating power

Confidence when submitting offers

The smoother your financing process, the smoother your home purchase.

Mortgage approval isn’t about perfection — it’s about preparation.

Understanding what lenders look for allows you to position yourself strategically and avoid unnecessary delays.

If you’re considering buying this year, having a conversation early with both a real estate professional and a trusted lender can help you move forward with clarity.

Stay up to date on the latest real estate trends.

Real Estate News

First impressions matter more than you may think when selling your home

Understanding the factors that may be preventing buyers from making an offer

Seller's Guide

Understanding the pros and cons before making a decision

Seller's Guide

Why pricing your home correctly is one of the most important decisions you'll make as a seller

New Listing

Unobstructed Ocean Views from One of San Clemente’s Most Coveted Bluff-Front Locations

Our team is ready to handle every aspect of your transaction to facilitate the home buying, selling, commercial, or retail sale process. From the largest estate property to the first time buyer purchase, commercial real estate, and everything in between, we have the experience and knowledge to help.